It replaces political calculation with ROI calculation formulating decisions based on achieving a better return on investment.

Working over twenty five years in America’s financial sector for both large and small companies and now as the director of research and strategy for a $10 billion institutional investment fund manager, I have experienced firsthand what drives economic growth, what stimulates job and wage growth. And I’ve seen up close both how the financial sector operates and its role within the economy. My experience also includes advising the Chicago and Washington, D.C. districts of the U.S. Federal Reserve as well as CalPERS, the largest U.S. public pension fund.

Stock market prognostication is something I typically highly recommend against doing, yet I do so below. Why?

First, because I perceive an unusually high level of risk in today’s equity markets. This is based on the inconsistency between today’s stock market valuations on the one hand and on the other hand today’s depressed economic environment and especially because of the highly uncertain vaccine development and distribution timeline.

Second, because the risks inherent in today’s equity markets so far have not been appropriately highlighted in the financial media outlets targeting investors.

If after reading below you are more aware of the heightened risk

in today’s equity markets, the primary objective in writing this will

have been achieved. The predictions are secondary in importance as they

are merely the vehicle to communicate the risks in today’s equity

markets.

Stage 1: Frenzy

Equity Market Frenzy

Equity markets have been in a frenzy since their March nadir. As of the market close Friday the 19th,

the NASDAQ index is above, yes above, its February peak. The S&P

500 is less than 10% below its February high while the DJIA is within

12% of its high. This occurred in four short months after the February

peak in an environment of historic job losses, double digit

unemployment, and ongoing weekly million plus unemployment insurance

claims.

Consumer Frenzy

Shelter at home policies combined with consumers’ initial respect for

the risks associated with COVID-19 left consumers in a state of

isolation and economic hibernation. After numerous weeks of isolation,

some consumers couldn’t take it anymore and left their homes with great

enthusiasm creating a frenzy of activity.

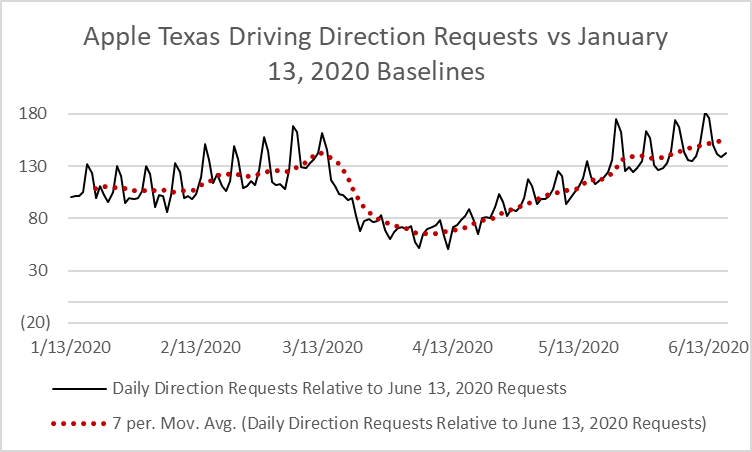

After seeing its average weekly requests for driving directions cut by 1/3 in Texas, Apple driving direction requests surged subsequent to the reopening and as of June 19th stand at 155% of pre-pandemic levels.

Source: Apple Mobility data

Economic Frenzy

Not surprisingly, increased consumer mobility led to increased

economic activity. Retail sales rebounded 17.7% in May. Consumers used

their newfound freedom to purchase automobiles, increase home buying,

and gleefully return to Las Vegas casinos. Topping it all off, initial

estimates indicate that a surprising 2.5 million jobs were added in May.

These all supported the view held by some economists that the best

analogy for the pandemic is a natural disaster and the view that the

economy will similarly bounce back quickly.

Stimulus Frenzy

Adding to the frenzy, fiscal and Federal Reserve stimulus has been

unprecedented and received with both relief and glee. Consumers lined up

to deposit their stimulus checks while unemployment insurance

recipients gave thanks for the increased size of their weekly benefits.

Vaccine Frenzy

After initially reporting the sobering opinions of experts that even

in a best-case scenario a vaccine would take 18, maybe 12 months to

develop a new, more optimistic story appeared. Reports that a vaccine

might be developed by the end of the year and available in 2021 began

dominating the news. More recently, some are even speculating a vaccine

might even be found by the presidential election.

Media Frenzy

Meanwhile, on-air stock market pundits and guests were validating the

fiscal and Federal Reserve stimulus frenzy as they confidently

proclaimed, “Don’t fight the Fed”, all while the outlets prominently

displaying their “street cred” to bolster the proclamations reassuring

viewers that now was the time to be in the market.

Media outlets have been scouring economic indicators for any positive

signs or even just less bad economic news and writing articles filled

with talk of an economic bottoming and multiple variations of headlines

along the lines of, “Signs of a V-Shaped Recovery”.

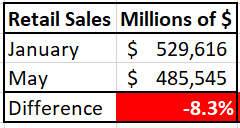

They hailed the 17.7% increase in retail sales hoping to bolster

consumer sentiment and investor confidence. This was done with very

little if any mention of the reality that retail sales remain down more

than 8% from their pre-pandemic levels, and rarely asking if May’s rate

of rebound was sustainable.

Source: U.S. Census Bureau

They reported on the slight rise in consumer sentiment while often

not mentioning that consumer sentiment remains very depressed.

Source: University of Michigan

Stage 2: Fear

While infection rates are improving in areas of the country hit

hardest first, infection rates are surging in many other states. The

surge in infections seemed to catch Wall Street off guard with stocks

declining nearly 7% on June 11th (only to be largely shrugged off in

subsequent days). This was despite basic logic showing the inevitability

of the resurgence in infection rates: If reduced circulation of people

resulted in reduced rates of infection…increased circulation of people

would result in increased rates of infection.

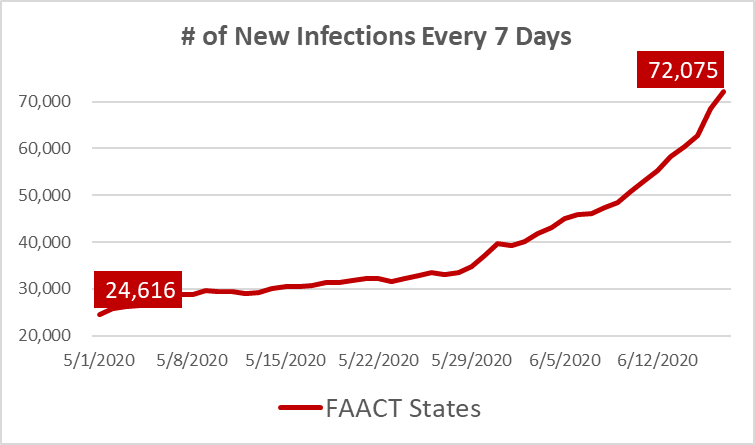

How bad is the resurgence in infection rates? Let’s look at the

FAACT’s, the FAACT states that is. These are what I call the FAACT

states: Florida, Arizona, Alabama, California and Texas. They

collectively have seen a near tripling of their seven-day infection rate

rising from under 25,000 cases before the reopening to more than 72,000

cases as of the last seven days. These five states alone now comprise

45% of total weekly U.S. infections, up from 12%.

Resurgent infection rates have resulted in fear-laden headlines

including among others, “Experts weigh in on which states are primed to

be the next COVID-19 hot spots” and “Texas announces record number of

hospitalizations as its daily death toll rises”.

Source: USA Facts

Stage 3: Fizzle

From Merriam-Webster: Fizzle – to fail or end feebly especially after a promising start

Note that the factors below underpinning my expectation for an

economic fizzle after a short-lived rebound do not include a second wave

of infections in the fall. If a substantial second wave were to occur

in the fall without widely effective and widely available viral

treatments the economic fizzle could quickly transform into a freefall.

Factor 1. Reports of early signs of a strong economic rebound are misleading.

Focusing on the percentage change from depressed levels gives viewers

an incorrect perception of the health of the economy. First, the

comparisons are to highly depressed levels. Second, mathematically, even

a rebound equal in percentage to the decline leaves economic activity

well below the prior levels.

Factor 2. While some areas of the economy have been able to notch

healthy early recovery rates, that doesn’t mean the early rates of

recovery can be sustained.

The few early signs of an economic rebound are due to pent up demand,

not a strong consumer able to sustain the early rates of recovery being

trumpeted as signs of a “V” shaped recovery.

The number of renters paying with credit cards in May was up 58% from

February. Millions of Americans remain unemployed and/or with reduced

hours.

Factor 4. Fading fiscal and monetary policy stimulus benefits.

The economic benefits from government stimulus checks Americans

received will fade if not repeated as will the benefits of augmented

unemployment insurance benefits if they are not extended after their

scheduled July expiration. The passage of additional measures to support

consumer finances is a wild card given the November elections. We are

already hearing reports that members of Congress are questioning whether

additional stimulus is needed given the early signs of an economic

rebound while other members of Congress voice concerns that the

increased unemployment insurance benefit is holding back employment

growth. There is also the question of whether Congress will provide

support to state and local governments to forestall likely layoffs

resulting from budget deficits.

While Federal Reserve monetary stimulus got credit markets

functioning supporting both the economy and asset valuations (albeit

artificially), its ability to stimulate future economic growth is

uncertain. Just how much more impact can the Federal Reserve have on the

economy when the 10-year Treasury rate is already below 1%? I guess

they could push rates negative and even buy equities to maintain the

“wealth effect”. If it came to that, it would be a sign economic growth

had weakened severely.

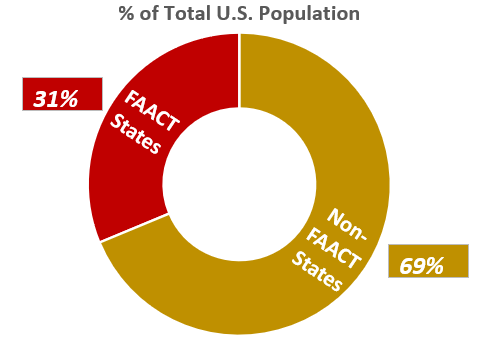

Factor 5. Economic impact of surging FAACT state infection rates.

The FAACT states contain nearly 1/3 of the U.S. population

They represent $6.8 trillion in GDP, nearly 1/3 of U.S. G.D.P

If businesses in these states are forced to again close their doors

or even curtail their operations, investors’ dreams of a “V” shaped

recovery could end abruptly.

Businesses are already closing their doors shortly after reopening

with Apple announcing it will close some stores it had reopened while

some restaurants including those in Texas are closing after reopening.

Source: USA Facts

Factor 6. Increasing business failures

While government programs for businesses have forestalled business

failures, not all businesses will be saved. Additionally, an increase in

businesses suspending operations in response to surging infection rates

would place additional businesses at risk of failing. Failing

businesses unable to repay their loans reduces the lending capacity of

financial institutions exacerbating the economic drag caused by failing

businesses.

Factor 7. Mortgage forbearance can’t last forever.

At some point lenders will need to either a. Be paid or b.

Acknowledge they won’t be paid. Without a sharp increase in employment

and borrowers’ ability to resume loan payments, lenders will need to

reduce the value of their loans reducing their capacity to lend

constraining economic growth.

Factor 8. Natural disasters are not good analogies to use as

basis for forecasting the possible economic recovery from the damage

done by COVID-19.

Some economists have sought reassurance in equating this pandemic

with a natural disaster. However, this pandemic is different from a

natural disaster in two crucial aspects:

1. While a natural disaster is typically isolated to one area of one country, this pandemic is

occurring globally.

2. While rebuilding often begins soon after a natural disaster with great force, current

economic rebuilding efforts are both tepid and vulnerable to significant setbacks.

Factor 9. End of year vaccine caveats

The hoped for and repeated reporting of a possible vaccine by the end

of the year often leaves off a key detail: The method being used to try

and develop a vaccine by the end of the year has never resulted in a

licensed vaccine during thirty-years of trying. Stories also may not

discuss the time it will take to manufacture the vaccine; let alone the

time it will take to get everyone vaccinated.

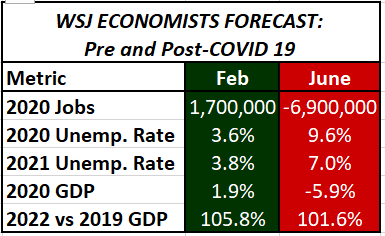

How likely is an economic fizzle? The table below compares the February and June Wall Street Journal

consensus forecast of economists representing the collective economic

outlook of over 70 economists. The outlook reflects more of an economic

fizzle than a sustained economic frenzy.

The economists on average expect 2020 to end with nearly 7 million

fewer jobs than the beginning of the year, an unemployment rate of 7% in

2021, and GDP not returning to 2019 levels until 2022.

Source: Wall Street Journal survey of economists

Stage 4: Fall

Yet, judging by the historic rebound in stock prices we saw

previously, investors seem to be ignoring this outlook. Instead,

investors seem be holding on to the hope for a “V” shaped recovery and

maintain hope that “This time is different” because this is more like a

natural disaster with fleeting effects, all while falling back on tropes

such as, “Don’t fight the fed” to justify today’s equity market

valuations in the face of tepid economic outlooks.

While hope-based valuations can be maintained for some time, hope is

not a firm foundation for valuations. This is especially true when

adding in highly unstable Investor sentiment. How unstable is investor

sentiment? Equity prices declined nearly 7% on June 11th alone, and that was during the frenzy stage.

At some point, if the hoped-for economic frenzy does turn into the

fizzle I envision, equity valuations will eventually decline to match

the reality of a slower economic recovery.

Now we wait and see what actually happens benefiting from a more complete view of the risks involved as we wait.

Stay in the know:

Receive unique insights into the economy, global trade, and financial markets you can use in investing, in your business, and evaluating Presidential candidate policies.

Read More

Read More